Introduction

In Singapore, many people turn to credit cards or personal loans for quick access to cash when life throws a financial curveball. From sudden car repairs to medical emergencies or wedding expenses that exceed the budget, these financial tools often provide an immediate safety net.

While both options offer convenience, the personal loan vs credit card decision is rarely straightforward. Each comes with different cost structures, repayment expectations, and long-term implications. Making the wrong choice may increase interest costs, stretch repayments longer than expected, or create unnecessary financial stress.

Understanding how these two borrowing options work is essential before committing to either. This article breaks down the personal loan vs credit card comparison in practical terms, helping you decide which option aligns best with your financial needs, repayment ability, and long-term stability.

Key Takeaways:

- Which is cheaper in the long run: personal loan vs credit card?

In most situations, the personal loan vs credit card comparison favours personal loans because they usually come with lower interest rates and fixed repayment schedules that reduce total borrowing costs over time.

- Is a credit card bad for borrowing money?

Credit cards are not inherently bad, but they are designed for short-term use. Long-term balances can become expensive very quickly.

- When does a personal loan make more sense than a credit card?

In the personal loan vs credit card decision, a personal loan is typically more suitable for large, planned, or unavoidable expenses that require structured and predictable repayments.

- Can I use both responsibly?

Yes. Many people combine both tools strategically, using credit cards for short-term spending and personal loans for major financial needs.

- How do I avoid debt problems when choosing a personal loan vs a credit card?

Understanding the differences in a personal loan vs credit card setup, planning repayments ahead of time, and borrowing only within your means are key to maintaining long-term financial health.

Personal Loan vs Credit Card: The Basics

What Is a Personal Loan?

A personal loan provides a fixed lump sum that you repay through equal monthly instalments over an agreed period, typically between one and seven years. It is commonly used for larger, planned expenses where knowing your exact monthly commitment helps with budgeting and financial discipline. This structure makes the personal loan vs credit card comparison relevant for borrowers who value predictability.

1. Fixed Repayments

Monthly instalments remain consistent throughout the loan tenure, which makes it easier to plan ahead and manage cash flow. As the repayment amount does not fluctuate, borrowers can factor the instalment into their regular expenses without worrying about sudden increases.

2. Lower Interest Rates

Personal loan interest rates are generally lower than revolving card charges, especially when compared to most credit card interest rates in Singapore. Lower rates mean a greater portion of each payment goes toward reducing the principal instead of servicing interest. Over time, this results in significantly lower total borrowing costs, particularly for larger loan amounts or longer repayment periods.

3. Transparent and Regulated

Licensed money lenders in Singapore are strictly regulated by the Ministry of Law under the Moneylenders Act, which requires them to disclose fees, repayment schedules, and interest calculations clearly upfront. This transparency allows borrowers to understand their full financial commitment before accepting a loan, reducing the likelihood of unexpected charges or misunderstandings later on.

Example:

You have just received the keys to your new HDB flat, and renovation costs are estimated at $100,000. Instead of relying on savings or multiple cards, taking a personal loan at an interest rate of 3.88% per annum (p.a.) over five years may result in monthly repayments of approximately $1,850. This approach keeps your cash flow stable while avoiding revolving debt.

When evaluating personal loans vs credit cards, a personal loan provides greater clarity and predictability. Combined with lower and clearly defined costs, its repayment model is more suitable for major financial commitments that require stability and long-term planning.

What Is a Credit Card?

A credit card offers revolving credit, allowing you to borrow repeatedly up to a set limit. Unlike personal loans, balances can fluctuate monthly depending on spending and repayment behaviour. Credit cards are designed primarily for convenience and short-term cash flow needs rather than long-term financing.

1. Revolving Credit

A credit card operates on a revolving credit basis, meaning your available limit is restored as you repay what you have spent. This allows you to reuse the credit line repeatedly without reapplying, making it suitable for ongoing expenses. However, the balance can carry over from month to month, thereby requiring careful monitoring to avoid accumulating debt unintentionally.

2. Flexible Repayment

Credit cards allow you to choose how much to repay each month. Paying the full balance by the due date allows you to avoid interest charges altogether and keeps borrowing costs low. Making only the minimum credit card repayment keeps the account active but leaves the remaining balance accruing high interest over time.

3. Rewards and Perks

Many credit cards offer incentives such as cashback, air miles, or reward points on everyday spending. These benefits can add value when balances are cleared promptly, but they should not drive spending decisions. If interest accrues, the cost of borrowing often outweighs the value of the rewards earned.

Example:

After covering renovation costs with a fast personal loan in Singapore, you might still need funds for furniture or appliances. Using a credit card for these smaller purchases can be practical, especially if you repay the balance quickly.

In the personal loan vs credit card discussion, credit cards excel in flexibility but demand discipline to avoid high interest costs. Without careful repayment planning, balances can accumulate quickly and become expensive to manage.

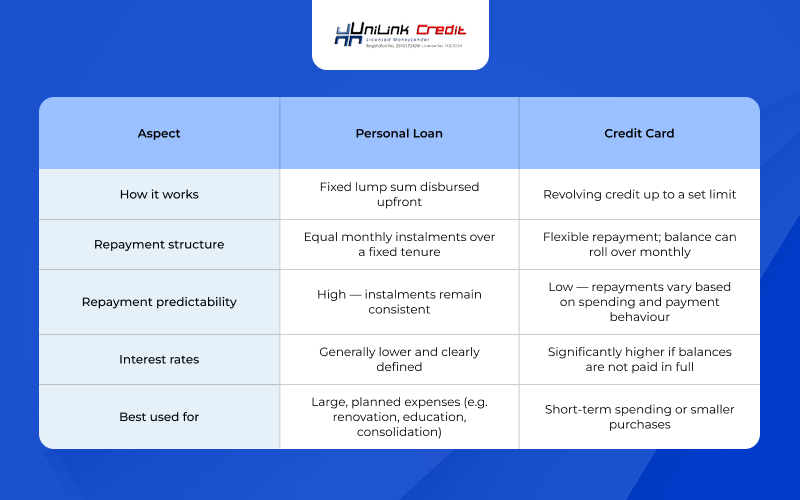

| Aspect | Personal Loan | Credit Card |

|---|---|---|

| How it works | Fixed lump sum disbursed upfront | Revolving credit up to a set limit |

| Repayment structure | Equal monthly instalments over a fixed tenure | Flexible repayment, balance can roll over monthly |

| Repayment predictability | High – instalments remain consistent | Low – repayments vary based on spending and payment behaviour |

| Interest rates | Generally lower and clearly defined | Significantly higher if balances are not paid in full |

| Best used for | Large, planned expenses (e.g. renovation, education, consolidation) | Short-term spending or smaller purchases |

Personal Loan vs Credit Card: Which is Better?

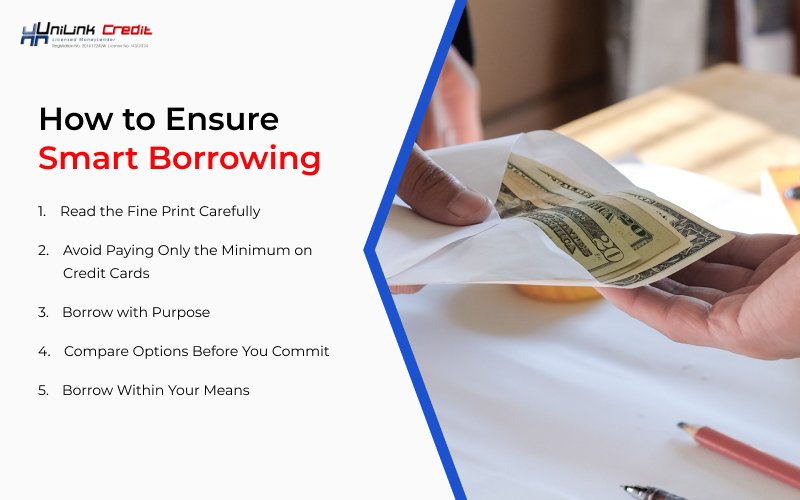

How to Ensure Smart Borrowing

Making informed borrowing decisions plays a critical role in preventing long-term debt issues and financial strain. While weighing personal loan vs credit card often focuses on interest rates or convenience, the more important consideration is how well the borrowing option aligns with your financial situation and repayment capacity.

1. Read the Fine Print Carefully

Loan agreements differ in how interest is calculated and what fees apply. Always check whether rates are flat or based on a reducing balance, and note any late payment charges. Understanding these details helps you estimate the true cost of borrowing over time and reduces the risk of unexpected charges.

2. Avoid Paying Only the Minimum on Credit Cards

Minimum payments may appear manageable, but they often lead to prolonged repayment periods and substantial interest accumulation. A large portion of each minimum payment goes toward interest. Over time, this can result in paying far more than the original amount borrowed.

3. Borrow with Purpose

Borrowing should serve a clear, necessary purpose such as education, healthcare, or home improvement. Impulse spending financed through borrowing often creates regret later. Understanding the personal loan vs credit card difference helps ensure the borrowing option matches the purpose of the expense. When borrowing is tied to a defined goal, it becomes easier to plan repayments and stay disciplined.

4. Compare Options Before You Commit

Taking time to compare personal loan and credit card offers helps you identify the most suitable structure and cost for your needs. Interest rates, fees, and repayment flexibility can vary widely across providers.

5. Borrow Within Your Means

Responsible borrowing requires aligning repayment commitments with your income stability and lifestyle needs. Keeping repayments within a manageable range helps maintain long-term financial balance and flexibility.

When a Credit Card Might Work

With these borrowing principles in mind, it becomes easier to assess which option fits specific situations more appropriately. In this section, we look at when using a credit card can make practical sense, provided it is managed carefully and aligned with short-term financial needs.

Credit cards can be effective financial tools when used in the right situations:

- Everyday expenses such as groceries or transport

- Short-term purchases that can be repaid quickly

- Earning rewards when balances are cleared monthly

Key Reminder:

Credit cards are designed for short-term convenience. When used as a substitute for a personal loan, interest can compound at rates of up to 26.9% p.a., causing balances to grow quickly and erode financial stability. In the personal loan vs credit card comparison, this risk becomes clear when balances are carried over for extended periods, turning convenience into a costly repayment burden.

When a Personal Loan Is the Smarter Choice

While credit cards can be useful for short-term needs, they are not always the most practical option for larger or longer-term financial commitments. When deciding on a personal loan vs a credit card, personal loans are often more suitable as they provide structured repayments and clearer cost control.

Personal loans are better suited for substantial expenses, such as:

- Major life events like weddings or education

- Debt consolidation loans

- Emergency funding where high interest must be avoided

In many personal loan vs credit card scenarios, personal loans offer greater clarity and structure, helping borrowers stay disciplined and avoid debt spirals. While credit cards are designed for convenience, using them for long-term borrowing can result in compounding interest of up to 26.9% p.a., turning short-term flexibility into a costly repayment burden.

Why Personal Loans Are a Better Safety Net

Unexpected emergencies can place immediate and significant strain on your finances, especially when costs are high and timing is critical. In situations such as medical procedures, urgent household repairs, or sudden income disruptions, the priority is securing funds in a way that remains manageable over time. This is where the personal loan vs credit card distinction becomes especially important, as personal loans often provide greater stability and cost control during periods of financial stress.

Advantages:

- Access to higher loan amounts at manageable rates

- Fixed repayment schedules that reduce uncertainty

- Lower total interest compared to revolving debt

Example:

Borrowing $12,000 through a low-interest personal loan in Singapore at 3.88% p.a. over three years results in predictable monthly repayments. It also leads to significantly lower total interest compared to carrying the same balance on a credit card.

Frequently Asked Questions

1. Can I apply for a personal loan if I have multiple existing credit cards or loans?

Yes, you can apply for a personal loan even if you have other financial commitments. In the personal loan vs credit card context, lenders focus on your overall debt burden and repayment capacity, so having a clear income record and manageable obligations may improve your chances of approval.

2. Are there early repayment penalties if I pay off my personal loan ahead of schedule?

No. Legal money lenders in Singapore cannot impose a penalty solely for early repayment. Paying off your loan early can reduce interest costs and is generally encouraged, provided the contract terms allow for it.

3. How much can I borrow for a personal loan from a licensed money lender?

Borrowing limits depend on income level and regulatory caps designed to support responsible borrowing in Singapore. For unsecured loans, the amount you may borrow from all licensed money-lenders combined is up to six times your monthly income if you earn above the threshold. There are lower caps for lower-income brackets.

Conclusion

The personal loan vs credit card decision ultimately comes down to purpose and repayment discipline. Personal loans offer structure, predictability, and lower costs for significant expenses, while credit cards provide flexibility for short-term needs when managed carefully.

Planning in advance, comparing options thoroughly, and understanding how interest accumulates are essential steps before borrowing. Knowing how to borrow money legally in Singapore also ensures protection under local regulations and avoids unnecessary risk.

If you are seeking guidance from a trusted money lender in Singapore, Unilink Credit can help you assess your options responsibly and with clarity. As a member of the Credit Association of Singapore, formerly known as the Moneylenders Association of Singapore, we follow recognised industry standards and responsible lending practices.

Reach out today to discuss a solution that fits your financial needs without unnecessary strain.